A modern, risk-free path to solar ownership is Prepaid solar leases & PPAs. Enjoy predictable costs, hassle-free installation, and long-term energy savings while embracing clean, renewable energy for your home. Learn how they are transforming solar ownership while maximizing long-term savings.

Installing a solar energy system is a costly investment, but the good news is that there are several solar financing options to fit your budget and financial goals. Lets explore each financing option and its pros and cons to help you in the decision-making process.

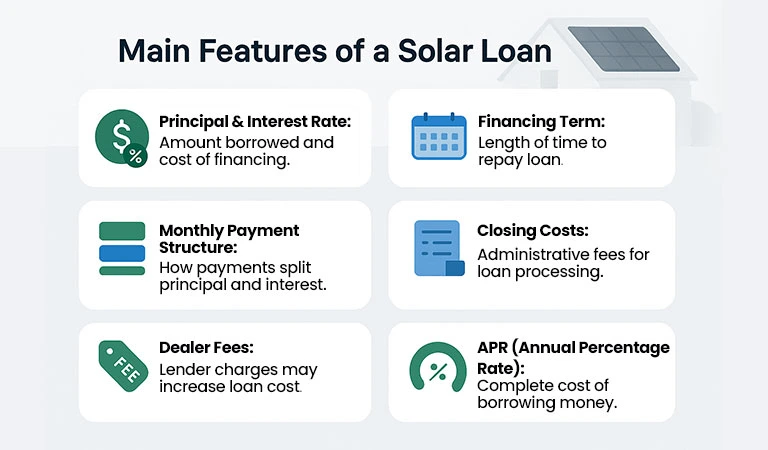

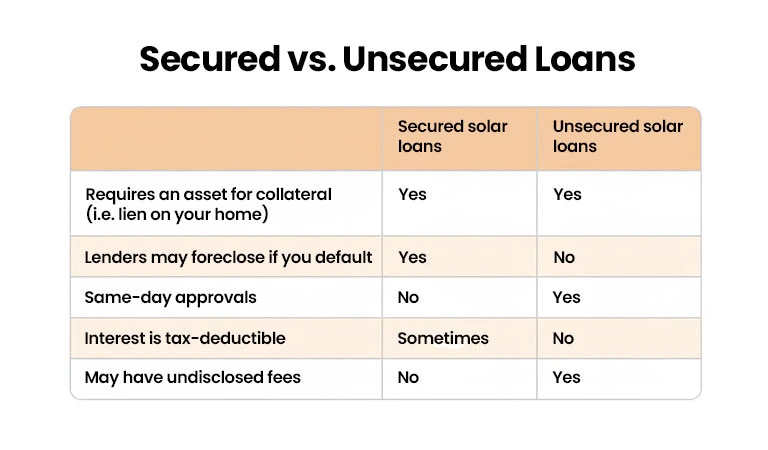

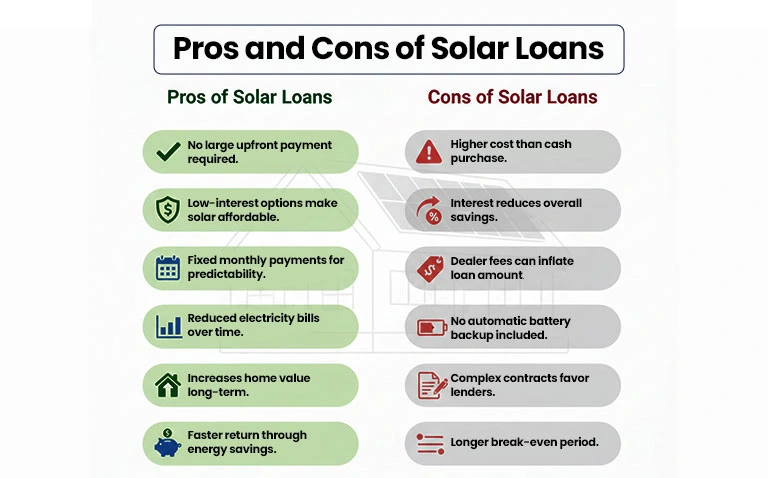

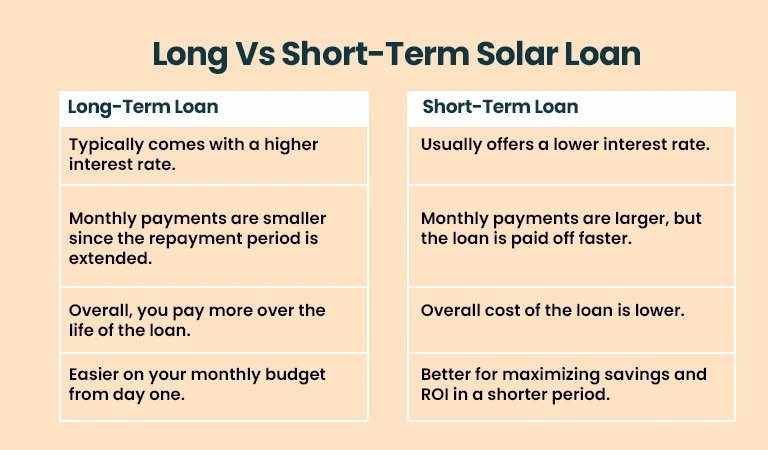

Solar loans are a cost-effective solution for installing solar panels on your home or business. However, many are unsure about their functionality and the benefits they might derive from this type of solar financing.