US Solar Battery Market Sets Record with 12.3 GW Installed in 2024

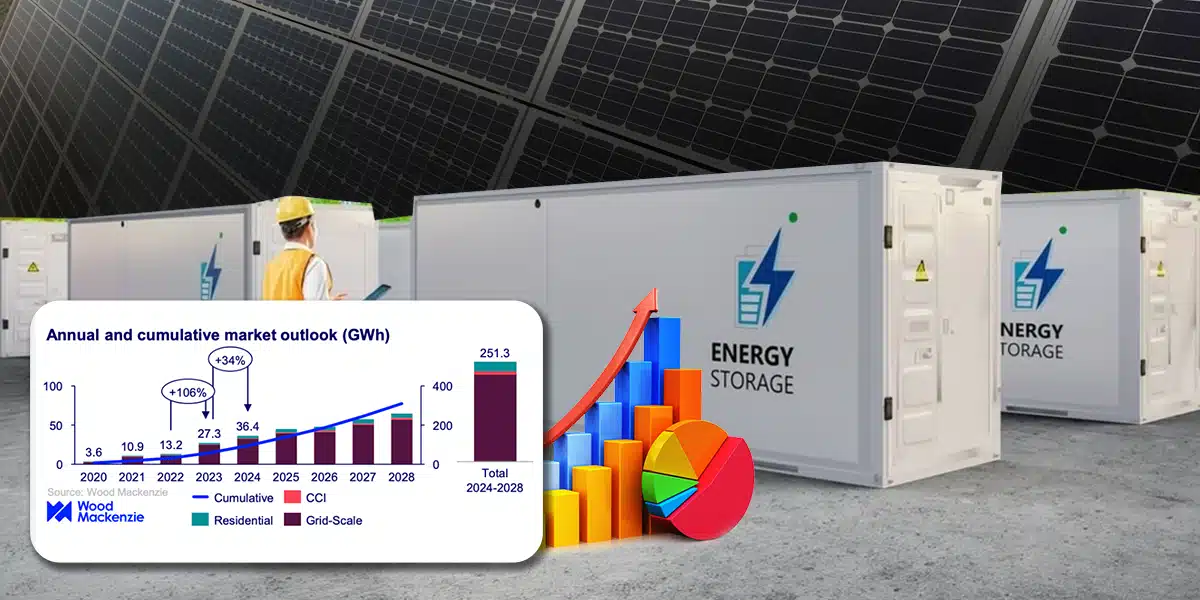

The US solar battery market is leading the way with a historical growth record in back-to-back years. According to the latest U.S. Energy Storage Monitor report published by Wood Mackenzie in collaboration with the American Clean Power Association (ACP), annual solar battery storage installations surged 106% in 2023 and 34% in 2024. Furthermore, the report forecasts it to reach 15 GW in 2025, representing a 25% increase over 2024.

The report reveals that the US installed 12.3 gigawatts (GW), or 36.4 gigawatt-hours, of energy storage capacity across all segments, including grid-scale storage, residential and commercial installations, in 2024, up from 27.3 gigawatt-hours in 2023.

Additionally, Texas and California remain the largest solar markets in the US, accounting for a significant portion of Q4 2024 installations. This impressive growth highlights a growing reliance on batteries for solar panels to support renewable energy and increase energy independence. The report covers 3 main sectors: big utility scales, home batteries, and battery storage for businesses.

Grid-Scale Battery Storage System Growth

Grid-scale solar battery storage systems continue to lead the way in the energy storage landscape. Although Q4 2024 installations were down 20% from the previous year, due to project delays. The US solar market set a record in 2024 with 12.3 GW deployment across all segments, representing a 34% increase. Grid-scale storage installations are promising to reach 13.3 GW in 2025. Texas and California lead the energy storage market, accounting for 61% of the total installed capacity in Q4 2024. Meanwhile, New Mexico and Arizona were the top contributors in Q4 2024.

Residential Solar Battery Growth

Residential battery storage hit a record in 2024, with over 1250 MW installed, an increase of 50% from the previous year. These stats highlight that residents turned to home battery storage for their energy needs. Furthermore, the residential battery installers had set the record quarter in Q4 2024, increasing 6% over the previous quarter by installing 380 MW. States like California, Arizona, and Texas installed energy storage systems the most because of frequent power outages, favourable policies, and awareness of renewable energy.

CCI Battery Storage Growth

The US Community, Commercial, and Industrial (CCI) battery storage market installed 145 MW in 2024, setting a 22% increase over the previous year. Based on the 22% year-over-year growth, the CCI Solar battery installations in 2023 were 119 MW. With 88% of installations, California, Massachusetts, and New York led the charge in the solar battery market. The forecast for 2025 anticipates the solar battery storage market will achieve 15 GW of installed capacity in 2025.

To conclude, after two historic growth years, solar battery is no longer a trend; it’s a part of the US energy future. As the interest in solar batteries is increasing day by day, the US solar battery market is set to make progress in 2025 and beyond. Whether you are a homeowner searching for a solar battery backup or a business in need of backup power. Now is the perfect time to install a solar battery storage system that meets your needs.

News Source: “U.S Energy Storage Monitor Report” by Wood Mackenzie